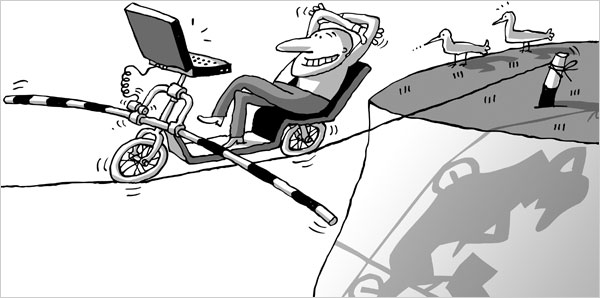

IF movies like "2001: A Space Odyssey" and "The Matrix" are any indication, humans are not comfortable with the idea of artificial intelligence controlling their fate.

So why ever trust a computer model to run your investments? Because, in the real world, it seems to pay off.

Many mutual funds that make their trades based on the recommendations of a proprietary computer model, known as quantitative or quant funds, have outperformed their benchmarks in the last three years. And investors have noticed.

At the Vanguard Group, which created its first such fund in 1985, the amount of money managed by its quantitative group has quintupled in the last three years, to $20 billion at the end of 2005 from $4 billion in 2002.

While no organization keeps track of flows into quantitative funds, they are probably still a very small part of the $9.5 trillion mutual fund industry. Many quant managers, however, say the funds' recent performance has received a lot of attention.

Quant funds can come in different flavors. Those like the Vanguard Strategic Equity fund, which is closed to new investors and was up 5.9 percent this year through June, let the computer model make practically all the decisions, from which stocks to buy and sell to when to trade them. Other funds, like the Quant Foreign Value fund, up 11.1 percent, use quantitative analysis as a screen to narrow down a basket of stocks. The final investment decisions in this type of fund are then made by carbon-based life forms.

Quantitative techniques emerged in the early 1970's and gave birth to the index fund in 1971, when Wells Fargo introduced a mutual fund that tracked 1,500 stocks on the New York Stock Exchange. As computer-processing power grew and more physicists and mathematicians left academia for Wall Street, money managers offered more robust services, and institutional investors began to embrace quantitative management for the advantages it offered.

The most obvious advantage is that quantitative models can examine a much larger universe of stocks than human analysts. Schwab Equity Rating, for example, analyzes about 3,000 stocks and assigns grades of A through F, based on four metrics: fundamentals, valuation, momentum and risk.

The expense ratios of quantitative funds are also generally smaller than those of comparable actively managed funds. And because the models have rankings of stocks, many employ short-term as well as long-term strategies.

But perhaps the most important attribute of quant funds is their superior risk control. Most models keep sector and equity picks within the benchmark attributes they are built around. This process reduces the risk that may otherwise be introduced by active managers who decide to make a bet on a particular sector or stock.

And that leads to what may be the most attractive aspect of a quantitative fund.

"With quant funds there is no emotion in the investment process," said Jeff Mortimer, head of equity portfolio management at Charles Schwab.

In other words, the investor is not exposed to the whim of an active fund manager who travels to a company's offices and whose investment decision may be partially based on his very complex, but unquantifiable, human experience while there.

A study published last year in The Financial Review found that enhanced index funds that use quantitative techniques outperformed their benchmarks, on average, from 1981 to 2000.

Still, it has taken longer for individual investors to embrace fully the idea of a "black box" running their investments.

It didn't help when, in 1998, Long-Term Capital Management, a hedge fund that bet on the predictions of its quantitative algorithm, suffered a spectacular implosion when its models failed to predict the Russian government would default on its debt.

And that leads to the biggest criticism of quantitative models: their reliance on historical data and their inability to assimilate new information quickly.

"It's not something that can be run on autopilot, despite the use of computer models," said Greg Carlson, an analyst at Morningstar, the mutual fund tracker. "You have to have a research team that's going to continue to look for new factors to add to the models because oftentimes the efficacy of a particular factor is either not recognized by the models or gets arbitraged away over time."

Mr. Mortimer of Charles Schwab said human managers at the company halted purchases of Merck in 2004 during the Vioxx controversy even though their models were calling for purchases of the stock. Merck's shares declined roughly 25 percent from the beginning of the problems through the second quarter this year.

There is another possible drawback of quantitative funds: because of the high volume of buy and sell signals generated by the models, the funds have higher-than-average turnover ratios and are therefore not as tax-efficient as index funds. This same factor also leads fund companies to limit the size of the funds.

Even though quant funds have performed well in recent years, Joel M. Dickson, head of Vanguard's active quantitative equity group, said investors should be careful about jumping into such funds now.

"I'm a little concerned that investors may be chasing performance," Mr. Dickson said. The most recent three years have been very good for many quant funds, he said, but he cautioned that their fundamental strategy may become less effective: as their stocks become more accurately priced, it becomes harder for quant managers to beat their benchmarks.

One of the best-performing funds so far in 2006 is the Bridgeway Ultra-Small Company fund, which uses five quantitative models to fill out its holdings with an assortment of growth, value and momentum stocks. The fund, now closed to new investment, gained 18 percent this year through June.

Still, it's rare to see a quantitative fund at the top of the performance charts, since many funds of this type aim only to outperform a benchmark.

But that has not deterred investors. Trying to capitalize on the new interest, mutual fund companies have introduced new quant funds in recent months.

Charles Schwab now offers 20 quant funds, 9 under the company's name, while the rest are managed by Laudus Rosenberg Funds. The Schwab Premier Equity Investor, which began in April 2005, was closed to new investors a year later. Schwab also recently started the Laudus Rosenberg International Discovery fund, which invests in international small- and mid-cap stocks.

VANGUARD started the Strategic Small-Cap Equity fund in April, bringing the number of its quantitative offerings to seven. The fund will use the Morgan Stanley Capital International U.S. Small-Cap 1750 Index as its benchmark.

In May, American Century Investments started three quantitative funds — Legacy Large Cap, Legacy Focused Large Cap and Legacy Multi Cap — bringing its total to 10. The funds are not bound by benchmark or sector restrictions and take greater risks.

"We don't actively monitor where we are all the time," said Sheila Davis, co-manager of the funds, "because if we did, it would make us want to do some things that the model tells us not to do."